Do visit the online store for products created by salvadordali the blogger. Here are a few of the items available.

https://salvadordali.clickasnap.shop/

Do visit the online store for products created by salvadordali the blogger. Here are a few of the items available.

https://salvadordali.clickasnap.shop/

|

| http://andropausesuccor.com |

|

| http://andropausesuccor.com |

I have written quite a bit on the said theme. Once you are convinced of a thematic play... it is best to use the "channel tunnel trading range" or swing trade. Pick the ones with the most beta and liquidity that suits your risk profile.

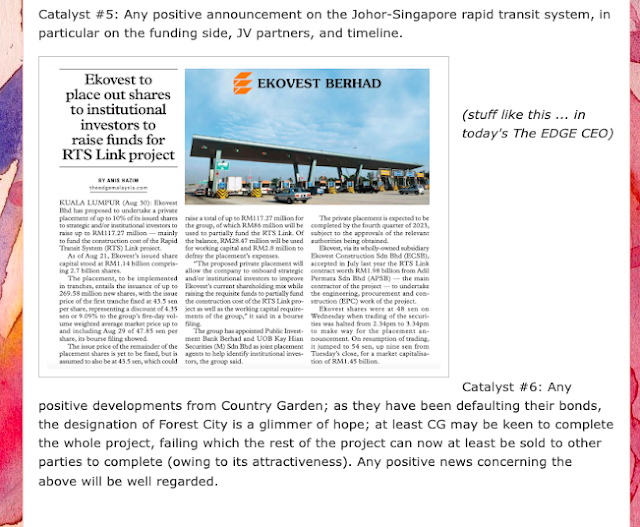

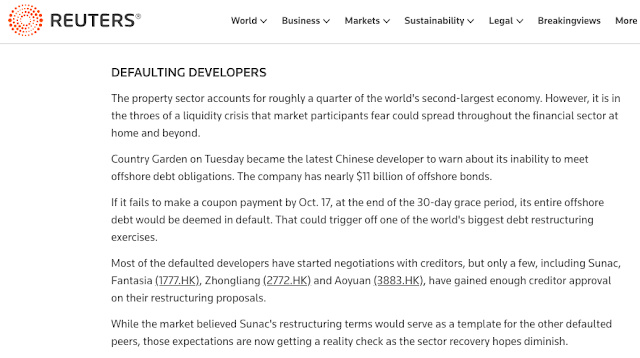

Today is Friday 13th .... look at Catalyst#6 ... on October 17th is a critical coupon payment of USD15 million that Country Gardens need to pay. That sum has already been given a 30 day grace period. So take that information to your trading strategy and act accordingly.

On the other hand, the upcoming Budget by PM may offer further positive newsflow to the theme. There should be sufficient volatility over the next 7 trading days.

For omakase, it is an overused term and concept. You are only getting produce the chef has ordered, so his links to suppliers (esp from Japan) is critical. Good Japanese food is not cheap.

That is why I don't get hung up with celebrity Japanese chefs. Next time you have an omakase or go to a famous sushi place, ask yourself, what are you paying for. Your RM400-1,000 has to pay for the expat chef's salaries, location, rental, service staff, etc. and after that produce.

(the salmon roe aged 5 days)

Chef Foo has garnered enough fans and followers to open at a 'dislocated' location because he is not going after walk in traffic. People will search for his place ... save a lot on rental.

(early appetiser, ebiko, fresh prawns, uni, topped with lavender petals)

(shima aji luxury roll with Japanese spring onions, ginger)

He is knowledgeable but is tied to the history of Japanese cuisine strictures. His selection is not tied to Edo (the old name for Tokyo) style sushi or Kansai-style sushi. Still, he has a deep respect for the cuisine and does not step much into the crazy Western style where fusion and almost anything goes.

(huge hotate, grilled lightly)

(the under-rated sardine)

(the aged otoro)

It is silly to try and call it the best, what I am trying to get at is the selection is often top notch and the cuts are generally premium cuts. There's enough interesting and hard-to-get stuff that serves as a greater charm to the whole meal.

They also do lunch sets, glorious ones too. Seating is limited to less than 15. Book before coming.